The Market is Challenging the Power of the Healthcare License

Success in a volatile environment requires health system leaders to keep a pulse on market dynamics and consumer and employee expectations.

Healthcare was built for stability, so it often fails to keep up with change—especially the volatility and uncertainty facing today’s industry.

Historically, healthcare was physically provided by licensed caregivers in licensed facilities. Just 10 years ago, value-based payment was essentially conceptual, telehealth had no government funding—and neither were a top priority for most organizations. Yet today, a growing 48% of Medicare enrollees are in Medicare Advantage (MA) plans, 69% of Medicaid enrollees fall under managed care contracts, and providers and payers are racing to attract members by offering the best digital and care-at-home experiences.1,2

The COVID-19 pandemic forced providers to respond to day-to-day needs, sparking more workforce shortages and burnout. It also generated opportunities for payers, private equity firms, and other innovators to invest in digital health, primary care, and additional network growth strategies – not just to close gaps in care but also to meet heightened consumer expectations. This has created a strategy gap, where the consumer-oriented playing field for payers and other companies with the means to invest in these services may yield more complete data and more satisfying healthcare experiences than licensees can undertake.

The Demand for Healthcare Services has Shifted

As opportunities for in-person care abruptly shrank in 2020, consumers demanded digital access to providers, and the industry responded with rapid-fire telehealth implementation, virtual innovation, care-at-home ecosystems, and advancements in technology. New ambulatory care and wellness options continue to proliferate alongside digital medical records and other virtual services, further empowering consumers to take control of their health, wellness, and treatment.

These fundamental changes are contributing to unpredictability in the demand for emergency room visits, inpatient volume, ambulatory surgery procedures, outpatient visits, length of stay, case mix index, virtual care, and more. In turn, almost universally, hospitals and health systems are facing financial and operational instability like never before.

Meanwhile, enterprise risks like cybersecurity have increased to a record high, hospital workforces are fragile, and price transparency regulations are elevating the need for reputation management and user-friendly, data-driven pricing tools.3,4 Additionally, the need to address social determinants of health (SDoH) has risen exponentially as many people experienced hardships due to the pandemic and as virtual care gave providers greater visibility into the factors that affect health.

Care Model Redesign is Already Happening

Startups are gathering seed funding for wellness apps and tech-enabled primary and specialty care based on consumers’ desire for on-demand access and more robust tools to manage their health. Startups like Homeward Health are tightly focused on underserved areas, such as rural communities.5 Others are exploring concierge-like approaches to primary care that build stronger connections with consumers.6>

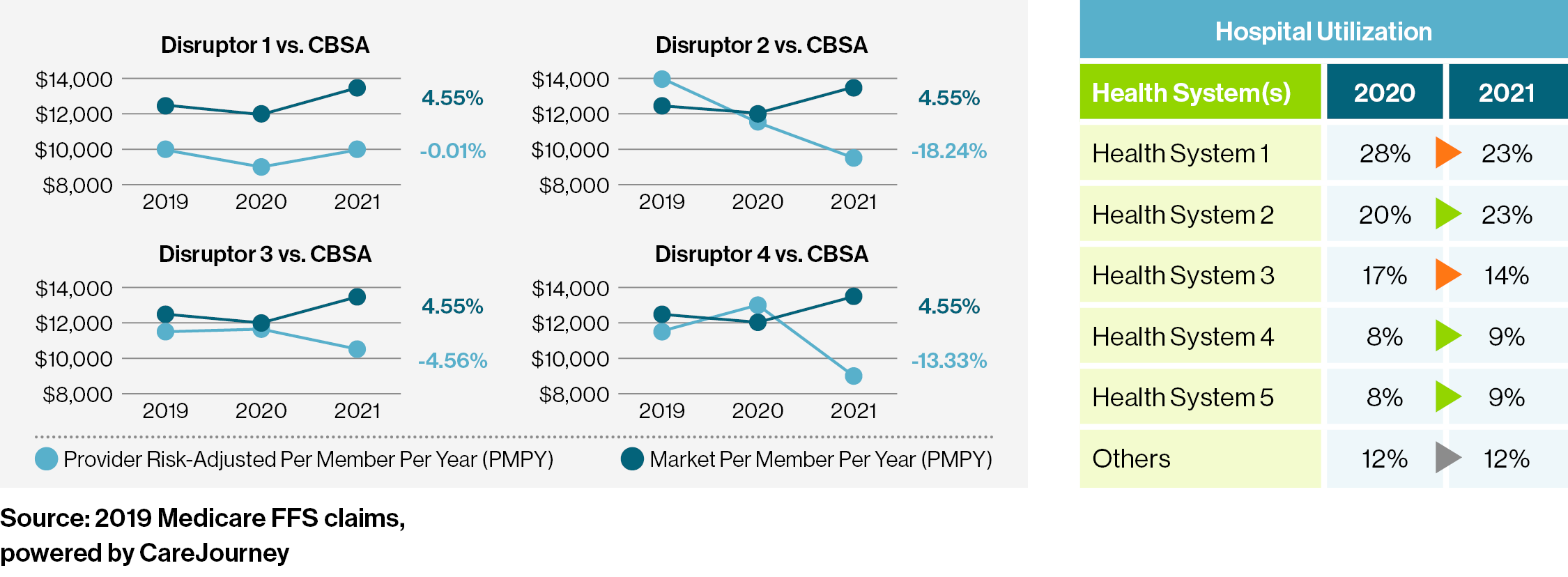

The common thread of success for these organizations is their ability to manage the total cost of care and steer patients to preferred health system partners that meet their clinical, financial, and operational expectations. A Guidehouse analysis of Medicare fee-for-service claims for four disruptor-based primary care groups in a large southeast U.S. city revealed that they were significantly outperforming the market on total cost of care and shifted facility utilization patterns by 13% from 2020-2021.

Likewise, payers are making big moves in primary and specialty care, with Humana planning to operate 260 health centers by the end of 2022 and Aetna ramping up acquisitions of primary care practices.7,8 Health plans are rebranding around “whole health” and partnering with clinical platforms and physician groups to shift more of their business into value-based payment models. With the ability to provide care at a lower cost than legacy providers, these partnerships are growing and make up an increasing share of primary care providers across large urban markets in the south and west.

Additionally, leading health plans are investing in early-stage companies to advance member enablement and engagement. Cigna put $450 million into its venture capital fund to drive innovation in analytics, digital health, and care delivery, while Blue Venture Fund—a collaboration between Blue Cross Blue Shield (BCBS), the Blue Cross Blue Shield Association, and Sandbox—targets investments in health tech, healthcare services, and life sciences.9,10

Moreover, within their core business models, health plans are laser focused on Medicare Advantage. They are capitalizing on MA economics by shifting Medicare expenditures from Parts A and B to rebate and bonus pools, largely achieved through provider performance, to fund enhanced customer benefits that will drive enrollment growth. In 2022, this amounts to $70 billion in rebate and bonus premiums, representing over $2,300 per beneficiary per year and an approximately 20% increase in their base Part A and Part B premiums.

There is also a notable rise in consumer-oriented companies partnering with payers and each other to drive down drug costs and strengthen access to urgent or primary care. In March 2022, Amazon Pharmacy announced a deal with five BCBS plans to integrate its drug discount card into coverage.11 Meanwhile, CVS Health has partnered with Uber and Lyft to address disparities in care by providing non-emergency medical transportation to target populations in certain cities.12

A New Strategy is Vital for Hospitals and Health Systems

For success amid the volatility, hospitals and health systems will need to further invest in meeting or exceeding consumer and employee expectations to garner their loyalty and trust. Here are five opportunities to consider for future growth.

1. Market Essentiality

Health system leaders need to reset their approach to excel in fee-for-service and value-based, alternative payment models, simultaneously. That means acquiring the comprehensive skills necessary for success in all care and payment models.13 This includes incorporating an active private equity element within their investment strategy to expand care settings.

Health systems are increasingly seeking adjacencies with other industry organizations, including pharma, home health, disease management, post-acute care, etc. Doing so will add the core proactive competencies needed to establish essentiality in the market with consumers, payers, purchasers, and clinicians and other critical workforce—optimizing performance under any payment model while hardwiring care coordination to improve patient experiences.

2. SDoH Infrastructure

Highly challenging economics have put nearly every health system “at risk” for their Medicaid patient populations, no matter their payment model. Coordinating care and engaging patients in the right settings of care can mitigate this challenge. Where and how a health system strategically engages with consumers leads to greater opportunities to coordinate care in their network, resulting in enhanced access, experiences, and outcomes. To do so, health systems need a SDoH-enabled infrastructure that understands community vulnerabilities, establishes strong relationships with community partners, and evaluates technologies with consumer equity in mind. Moreover, these strategies should be embedded within health system workforce expectations to ensure all stakeholders are satisfied.

It’s one thing to identify the unmet needs that impact a person’s health, such as when an individual indicates that they are facing food insecurity or housing instability. It’s another thing for a provider to know how to respond to those needs in the moment. As one physician told us, “It’s a terribly awful feeling to be looking at a patient who has attested to being housing insecure and not have the resources or community-based support to immediately be able to help that patient.

To get there, hospitals and health systems need to understand the true vulnerabilities that exist in their communities, such as through a community health needs assessment and review of data from community service agencies like United Way. Then, establish strong relationships with the agencies best suited to meet these needs so that the appropriate referrals can be made in the moment. Leaders also should consider channeling community health dollars and charitable investments to organizations that could have the greatest impact for those at risk.

Shifting workforce and team compositions to better meet community needs is another way to meet unmet patient and employee needs. For example, 87% of hospital CEOs plan to hire a broader range of talent to meet the needs of their communities this year.14 As organizations determine the best way to establish themselves as preferred providers, they may find they need fewer physicians to achieve these goals. Adding more social workers and case managers to the team could help take pressure off overloaded medical professionals while giving patients the right support in the right setting, including in the home.

3. Physician Strategy

In 2020, nearly 40% of doctors worked directly for a hospital or for a practice owned at least in part by a hospital, according to the American Medical Association. That’s up from 29% in 2012. Unfortunately, the deals didn’t meet volume, productivity, referral, and financial expectations. Meanwhile, consumers are choosing innovative primary care providers and disease management companies over their traditional health channels, resulting in material leakage to other providers.

A physician strategy that is in sync with the market dynamics of the new healthcare economy—emphasis on primary care; virtual care options; integrated behavioral care; digital sophistication; consumer and caregiver convenience and efficiency; competitive with new market entrants; willing to assume risk with those willing to share it—and completely aligned with an organization’s overarching strategic objectives is required.15

4. Workforce and Change Management

Labor is the root cause of delays in care delivery innovation. Clinician burnout, staff resignations, executive retirements, and equity issues now define many health system work environments. Fundamental changes in culture, work redesign, and workforce development are essential for providers to thrive in the new healthcare economy.

The characteristics of that new work environment include a culture of innovation, team-based care, and listening to multigenerational expectations, as well as a culture that prioritizes diversity, equity, and inclusion. This calls for an employment structure that offers a variety of work models such as remote and shared jobs, a clinical staff with an innovative mix of skillsets and licensures, and technology-enabled, streamlined workflows to increase productivity and retention.16

For example, there may be equity issues related to flexibility of scheduling for employees with hourly or shift-based work. This is especially true for women, who hold most shift-based positions and who were disproportionately affected by the pandemic, given disruptions in childcare, eldercare services, and more. Ultimately, equity issues related to staffing and compensation also affect the consumer experience because they limit the diversity of thought that goes into care decision-making and delivery. Focus on listening to staff to determine which workers are most at risk of leaving and their biggest pain points, then build the capabilities and resources to initiate change to address those concerns.

5. Technology Investments

Purposeful digital care and health IT investments are key to ensure they improve efficiency and the consumer experience, while streamlining corporate and non-clinical services. This means using technology to make life easier for consumers and clinicians.

For consumers, give people greater control in managing their healthcare experience. Consider how easily consumers can connect digitally with their primary care physician or a nurse—a major satisfier, given that 80% of consumers say they prefer digital interactions with providers.17 Then, examine the potential to close gaps in functionality or service using existing tech or with new solutions. For instance, if a patient were to face a complication related to a chronic illness on a weekend, would they be able to reach a member of the primary care team, or would a customer service representative direct that patient to “Call back on Monday when the office is open”? If the response is lackluster, it may hinder the relationship with that person. Evaluating new technologies and capabilities with equity in mind is also critical. Question whether investments will improve access to care, help reduce total cost of care, or improve quality.

Additionally, health systems cannot rely on their enterprise’s electronic health record (EHR) platform to create differentiation in user and patient experiences. Functionality built into EHRs is inherently a commodity, available to all users of the platform. Beyond ensuring they fully use their EHR's capabilities to avoid falling behind, the application layer needs to be managed on top of the EHR to create differentiation. This requires adhering to a more agile and rapid lifecycle than the norm and deploying a digital strategy based on an objective understanding of the organization’s opportunities and the emerging, but real, capabilities available in the market. The right technology, support, and processes for EHRs and other technologies can also help keep physicians and other clinicians from feeling disenfranchised, give them time back in their day, and promote an atmosphere of high reliability.18

Drive Financial Stability and Long-Term Growth

By exploring ways to keep pace with consumer and employee expectations, healthcare leaders can more effectively reset their organizations to build community relationships that last and drive financial stability and long-term growth. Guidehouse helps organizations modernize and innovate healthcare services, finances, and operations.

__________________________________________________________________________________________________

1 https://www.kff.org/medicare/issue-brief/medicare-advantage-in-2022-enrollment-update-and-key-trends/

2 https://guidehouse.com/insights/healthcare/2022/blogs/medicaid-marketplace-mcos-prove-worth

3 https://guidehouse.com/insights/healthcare/2022/blogs/cyber-in-healthcare-solutions

4 https://guidehouse.com/insights/healthcare/2022/blogs/price-transparency-complexities-in-2022

5 https://homewardhealth.com/

6 https://medcitynews.com/2021/03/concierge-primary-care-startup-forward-health-raises-225m/

7 https://www.modernhealthcare.com/insurance/humana-grows-private-equity-backed-primary-care

8 https://www.hartfordbusiness.com/article/aetna-parent-cvs-health-to-ramp-up-primary-care-expansion-eyeing-medical-practice

9 https://www.fiercehealthcare.com/payers/cigna-plans-invest-450m-venture-arm-digital-health-analytics

10 https://blueventurefund.com/

11 https://www.modernhealthcare.com/insurance/five-blues-plans-add-amazons-drug-discount-card-benefits

12 https://www.fiercehealthcare.com/digital-health/cvs-health-and-uber-health-partner-free-medical-transportation-to-reduce-barriers-to

13 https://guidehouse.com/insights/healthcare/2021/webinars/2021-clinical-integration-summit

14 https://guidehouse.com/news/healthcare/2022/cu-denver-guidehouse-survey

15 https://guidehouse.com/insights/healthcare/2022/6-ways-evolve-physician-strategy

16 https://guidehouse.com/insights/healthcare/2022/strategy-for-healthcare-workforce

17 https://www.forbes.com/sites/debgordon/2021/12/07/new-survey-shows-consumers-expect--better-healthcare-experiences-but-are-often-disappointed/?sh=7b8b638373f6

18 https://guidehouse.com/insights/healthcare/2022/blogs/ehr-optimization-critical